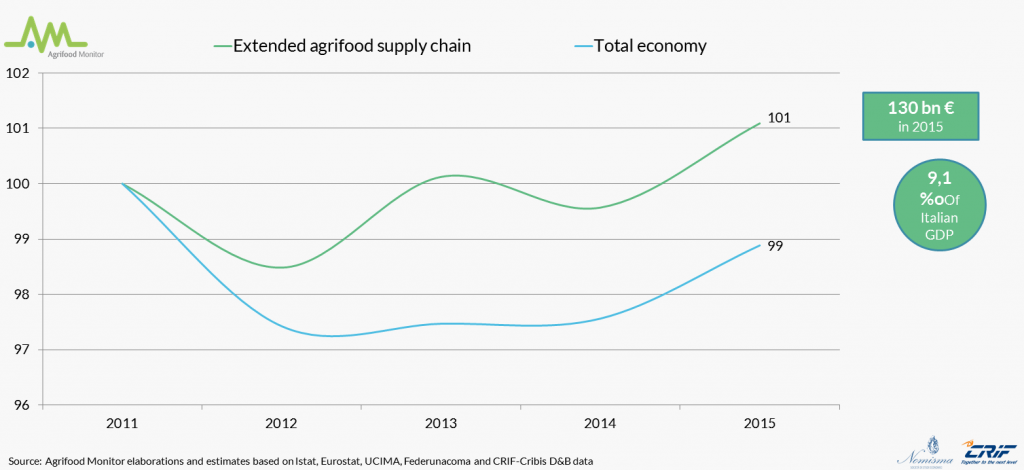

The extended agrifood supply chain is a very complex reality with a high number of businesses (about 2 million). On the one hand, they are committed to agricultural and food production, distribution, and marketing, on the other hand to manufacturing of machinery for the primary sector and the F&B industry. In 2015, all the operators of the agrifood industry generated a wealth of about 130 billion Euros and employed 3,3 million workers, ensuring a relevant contribution to the Italian economy: 9,1% of GDP and 13,5% of the employed population.

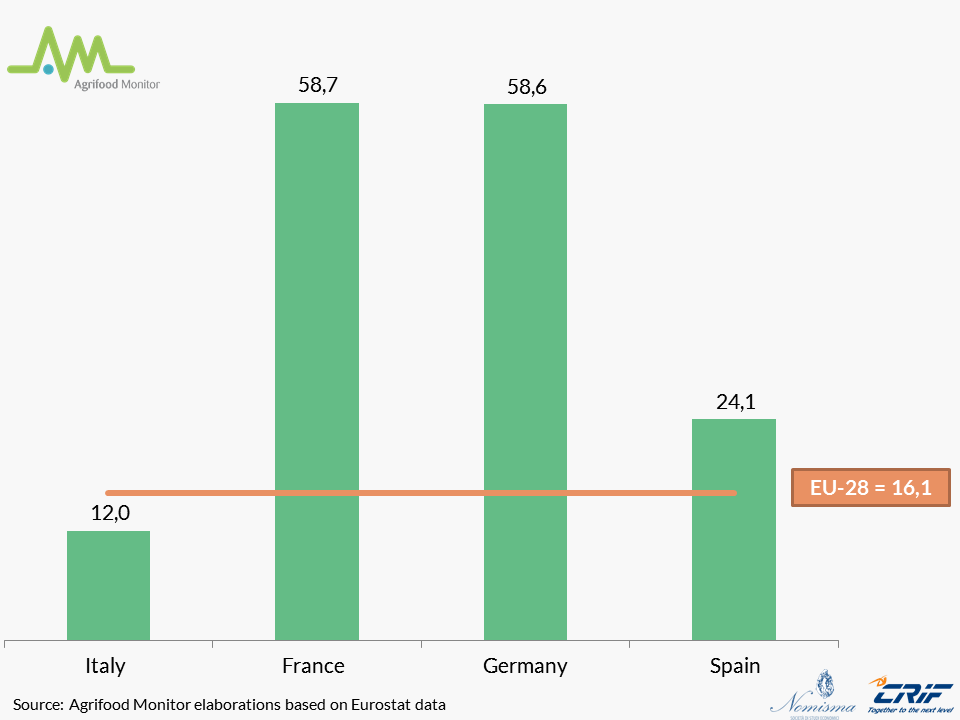

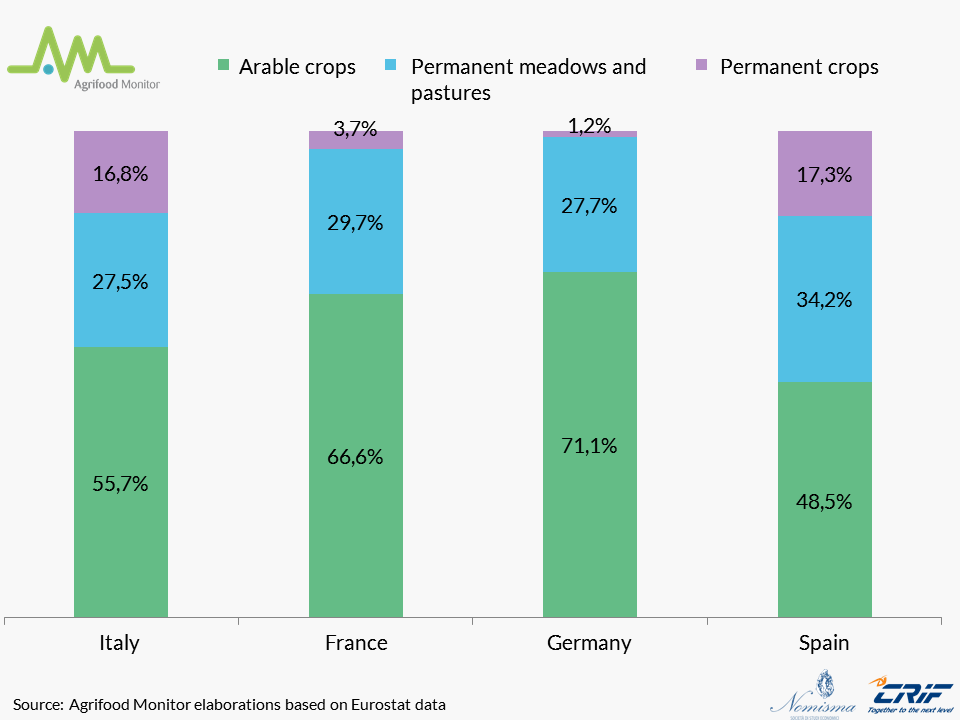

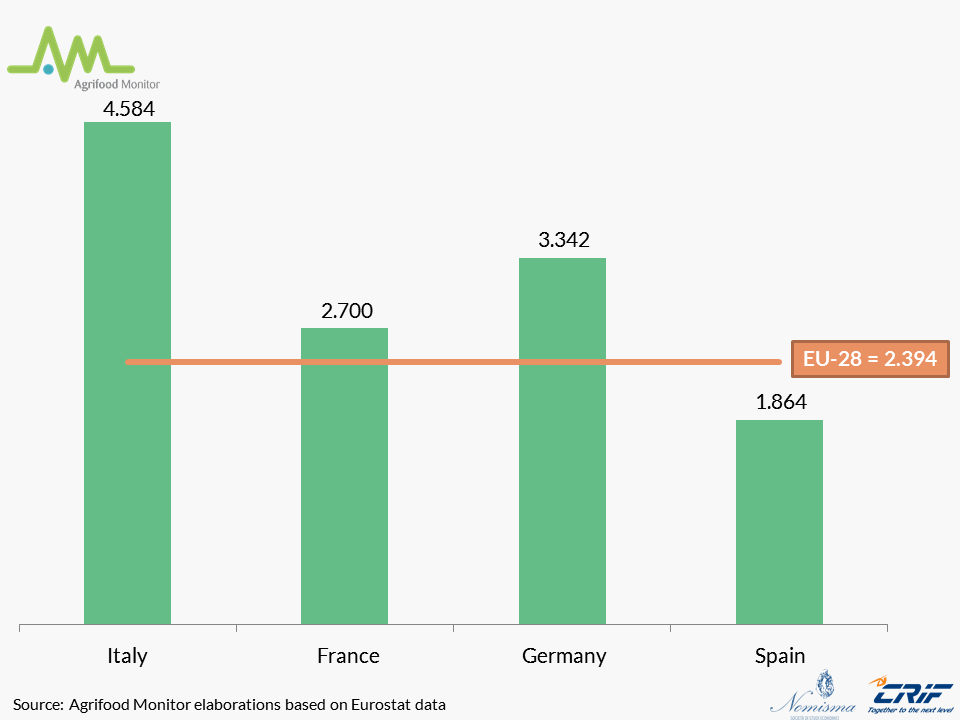

The average size of Italian farms is one of the smallest in Europe: 12 ha, approximately one-fifth compared to Germany and France. The productive specialization of the main European agricultural economies shows how arable crops prevail in the continental countries, whereas in the Mediterranean countries permanent crops have a significant role. Such a productive configuration obviously affects land economic performances: thanks to the productive diversification and the presence of high value added crops (such as fruit, vine, and olive), Italy registers a considerably superior land economic performance, not only compared to the European average, but also with respects to the main competitors.

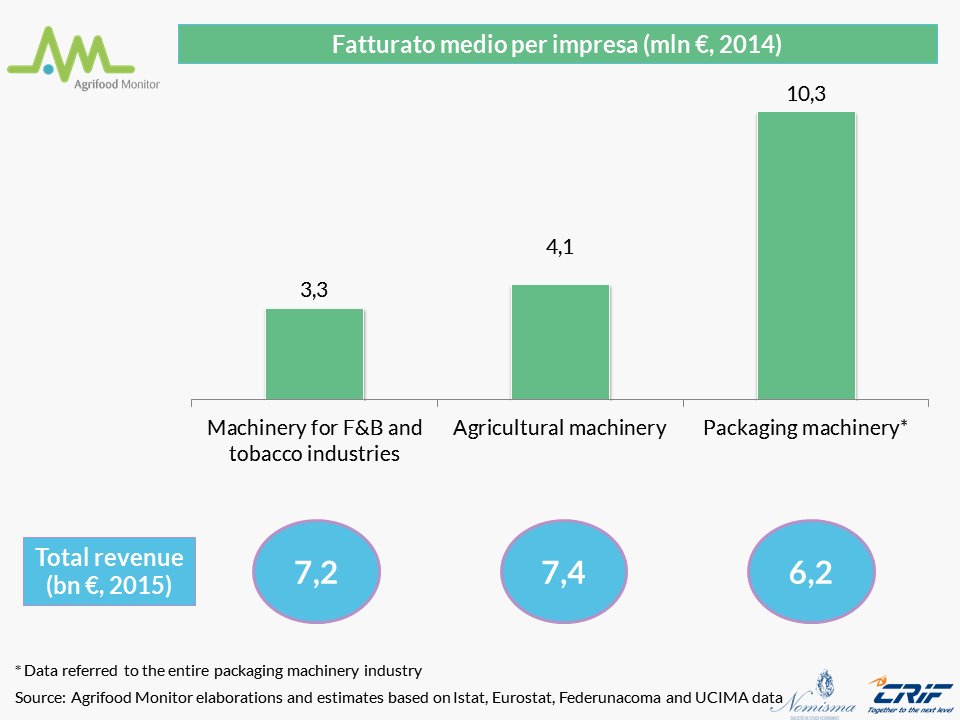

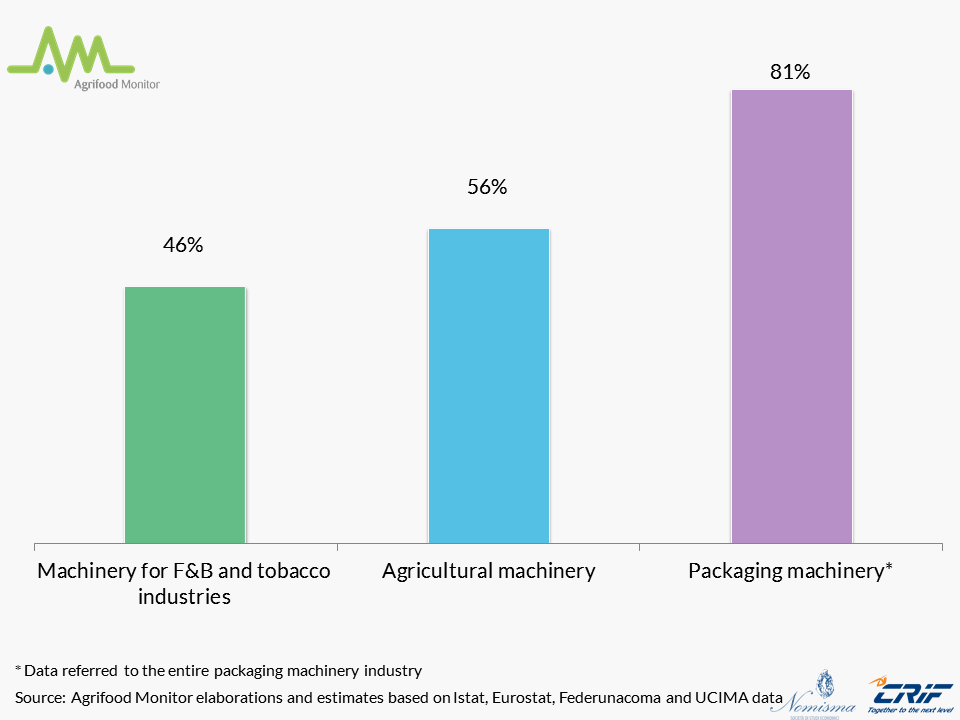

The production of machinery and equipment designed for agriculture and the food industry plays a prominent role within the Italian industry machinery: in 2015 indeed, about 18% of the industry revenue was generated by tractor manufacturers, F&B equipment manufacturers, and packaging machinery manufacturers. At the same time, the industry machinery is one of the most export-oriented Italian industries: the share of foreign sales on total revenue is about 46% for machinery and equipment designed for F&B industries, 56% for tractors and farm machinery, and above 80% for packing and packaging machinery.

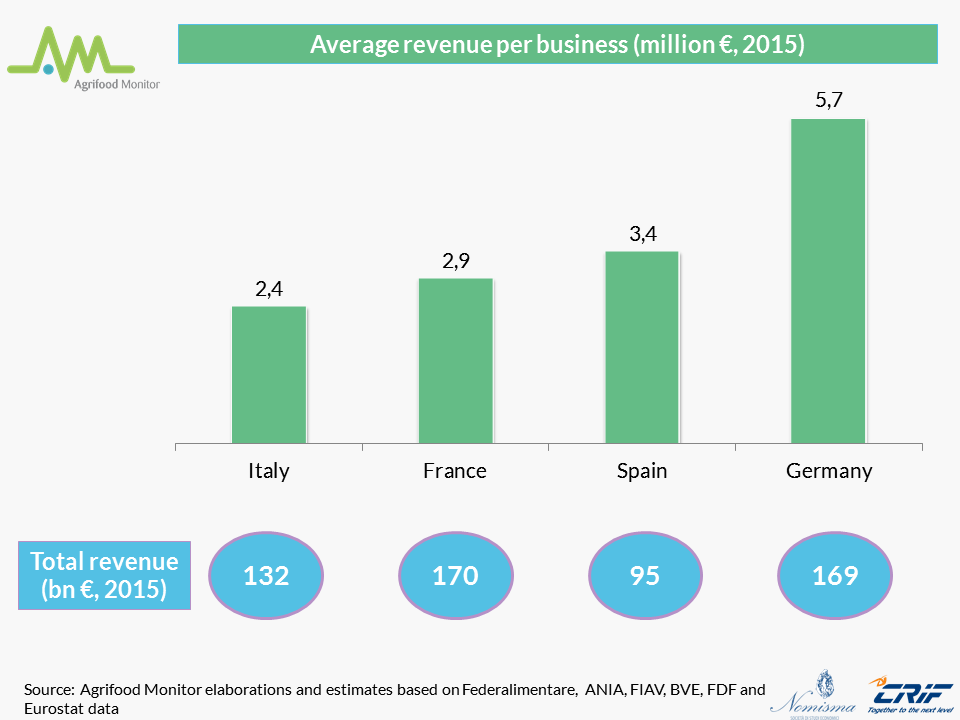

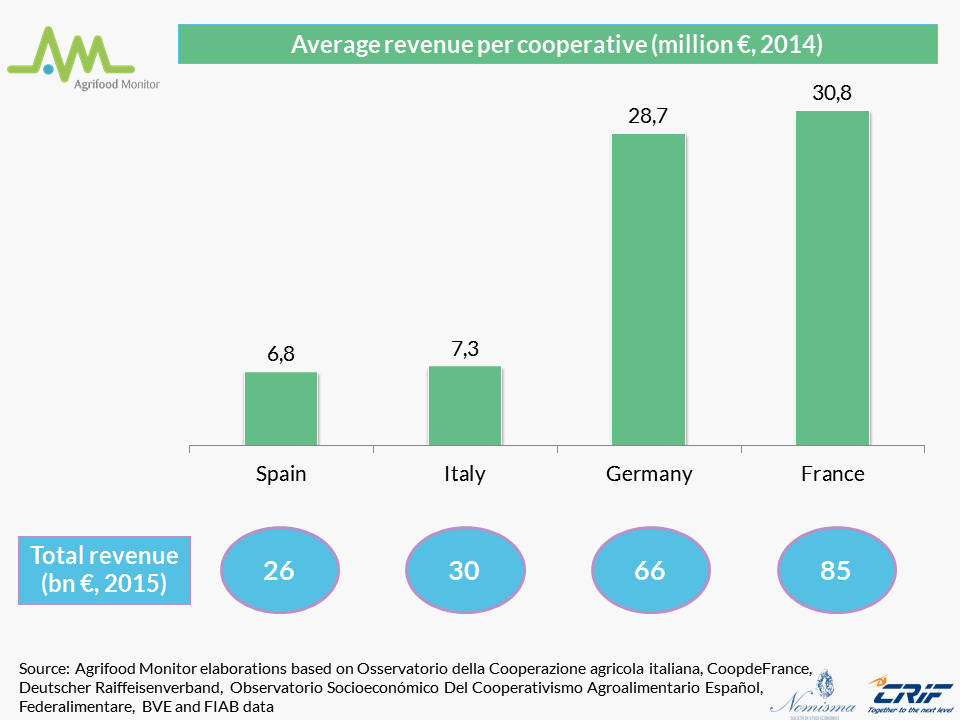

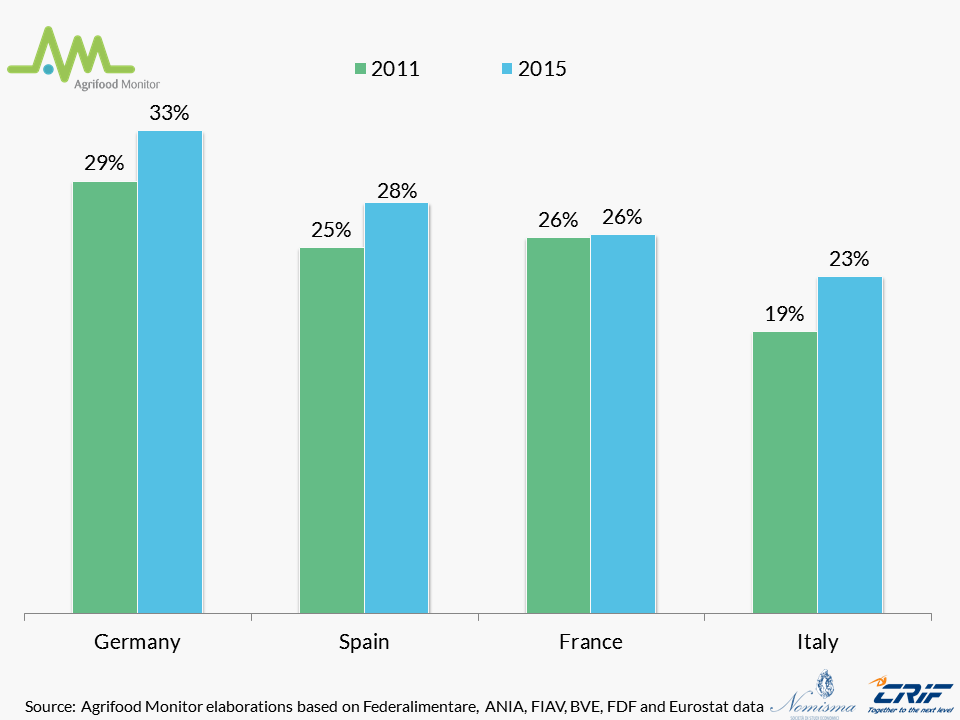

Even if the national food industry is one of the most important in Europe (132 billion of revenue in 2015), the Italian F&B manufacturing industry is small when compared to the main foreign competitors: the average size of the Italian businesses is indeed among the smallest in Europe, especially when compared to German businesses. The fragmentation of the industry is also confirmed by agrifood cooperation: thanks to their larger business dimension, France and Germany register higher revenue values than Italy (30 billion Euros in 2014), despite a lower number of cooperatives. The ability to access international markets seems to be closely related to business size: on average, F&B Italian businesses export 23% of their production (in value), whereas Germany 33% and Spain 28%.

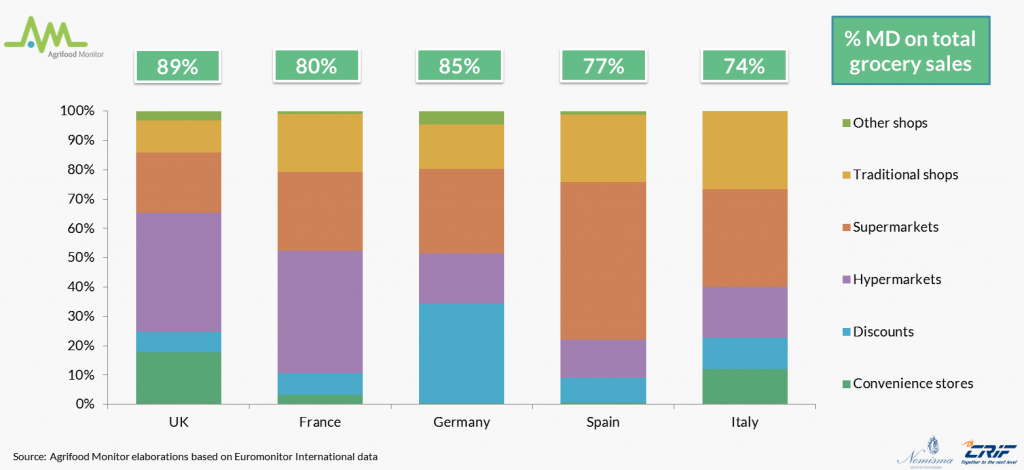

Large-scale retailing plays a key role in the marketing of food products both in Italy and abroad: in Italy, 74% of grocery sales (in value) takes place in supermarkets, hypermarkets, convenience stores and discount stores. This value is much higher in other European countries: more specifically, in Germany and the UK 85% and 89% respectively of food sales in the off-trade channel pertains to modern distribution.

Request free full version of the report in PDF format, in a few moments you will receive an email with the link.

All fields marked with *are mandatory.